For most students, financial factors are one of the biggest considerations when choosing a college. Many students ultimately decide where to enroll based on the financial aid package they receive.

The challenge? Financial aid letters aren't standardized. Every college presents information differently, uses different terminology, and may leave important calculations up to you.

Understanding what you're actually being asked to pay is essential before committing to a school.

This guide breaks down the key terms you'll see on financial aid letters and explains how to compare offers accurately.

Financial Aid Vocabulary You Need to Know

-

Some Financial Aid Letter Vocabulary

100% need-met schools: These schools meet 100% of the financial need they determine you have. Most are highly selective private colleges with large endowments, which allow them to provide generous financial aid packages. Keep in mind that different colleges calculate financial need differently, so aid packages can vary even among schools that meet 100% of need.

No-loan schools: These schools meet 100% of demonstrated financial need and do not include student loans in financial aid packages. Instead, they use grants and scholarships, helping students graduate with little or no debt. "No-loan" does not necessarily mean "free"—some families may still be expected to contribute toward college costs.

Grants and scholarships are free money; they do not need to be paid back. You want as much of your financial aid package as possible to come from grants and scholarships, since they reduce the amount you'll need to pay or borrow.

Loans are money that must be paid back. Before accepting a loan, find out:

- What the interest rate is — how much extra you'll pay over time.

- Example: A loan with a very high interest rate will cost much more in the long run.

- What the repayment term is — how long you have to pay it back.

- Example: A large loan with a short repayment period may result in very high monthly payments.

- What the monthly payment will be — make sure it's realistic based on your future income.

- How much you'll pay overall — always look at the total cost of the loan, not just the amount you're borrowing.

Federal loans: Subsidized vs. Unsubsidized

Many first-year students are offered federal Direct Loans ranging from $5,500 to $12,500 depending on year and dependency status. Federal loans are generally considered the safest loans to borrow because:

- The interest rate is fixed and cannot change.

- Federal loans usually offer better borrower protections and repayment options than private loans.

Subsidized loans are awarded based on financial need. The government pays the interest while you're enrolled at least half-time.

Unsubsidized loans begin accruing interest as soon as the loan is disbursed.

MAKE SURE you calculate both your monthly payment and the total amount you'll repay before accepting any loan.

FAFSA = Free Application for Federal Student Aid. You'll complete this during your senior year of high school to qualify for federal financial aid. The FAFSA becomes available each year on a schedule set by the federal government, so check current deadlines and submit it as early as possible. Many schools, libraries, and community organizations offer free help completing the FAFSA.

SAI (Student Aid Index) — This replaced the old EFC (Expected Family Contribution). Colleges use your SAI as part of determining how much financial aid you're eligible to receive. Your SAI is not necessarily what your family will actually pay for college.

Net Price Calculator — An online tool that estimates what you may pay at a particular college after grants and scholarships are applied. Search for the college's name plus "Net Price Calculator" to find it. These tools are helpful for comparing costs before you apply.

Loans can be declined — If you're offered loans that you don't want or need, you can choose not to accept them. Most colleges allow students to accept all, part, or none of their offered loans through an online financial aid portal.

Sticker Price (Cost of Attendance): The sticker price is the college's published cost before any financial aid is applied. It usually includes tuition, fees, housing, meals, books, transportation, and personal expenses. Very few students actually pay the full sticker price.

Direct Costs: These are costs billed directly by the college, such as tuition, fees, housing, and meal plans. Direct costs appear on your college bill.

Indirect Costs: These are expenses you may have while attending college that are not usually billed by the school, such as books, supplies, transportation, laundry, and personal expenses. Colleges often include estimates for these costs in their cost of attendance calculations.

Public vs. Private Schools: Private colleges often have higher sticker prices than public universities, but they frequently have more institutional aid available. As a result, some students pay less to attend a private college than a public university. Always compare net price, not sticker price, when evaluating financial aid offers.

- What the interest rate is — how much extra you'll pay over time.

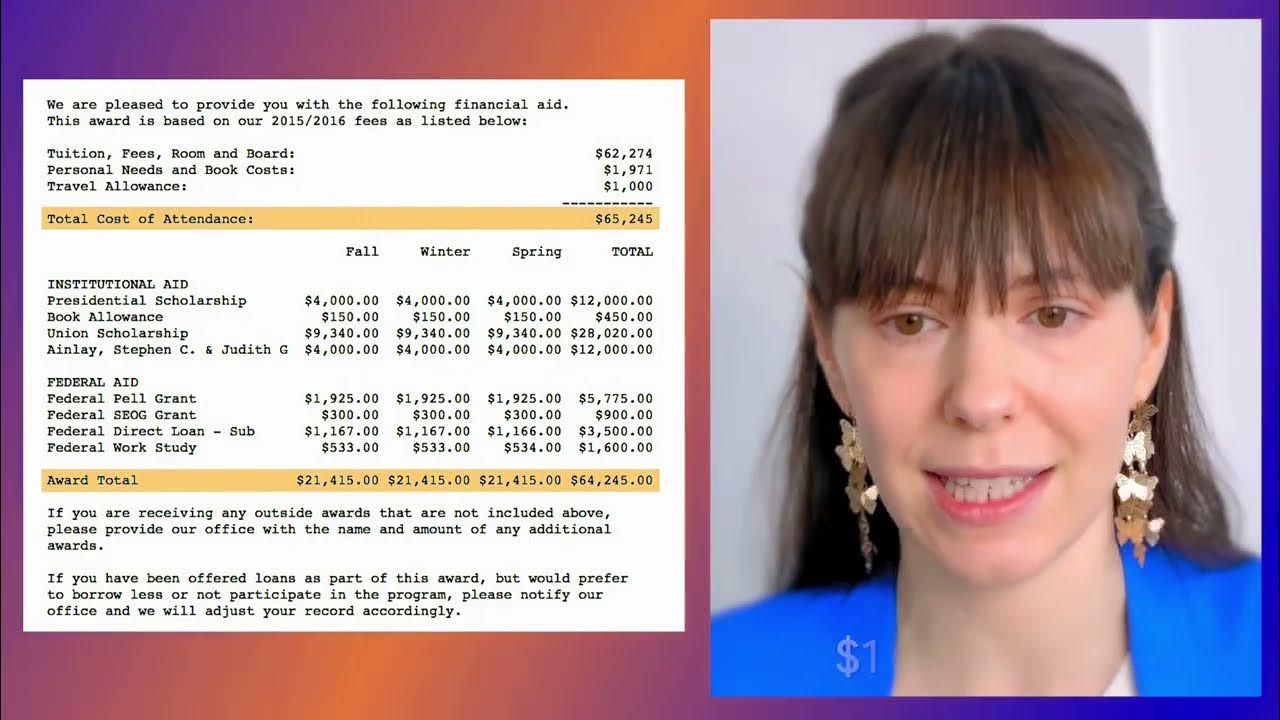

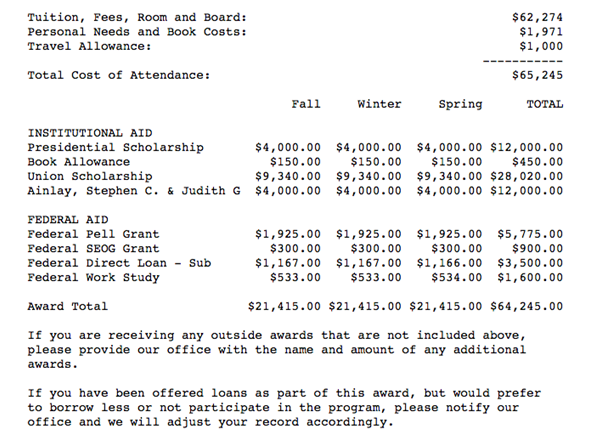

Full Ride Financial Aid Letter - college on trimester system that meets 100% of financial need

- Total cost of attendance = the whole price, all together: $65,245. Remember that not all colleges include room and board in this number and double-check that that’s included if you’re planning to live on campus.

- Gabbie got an allowance for books and travel — not all colleges will give this generously!

- But Gabbie lives in Florida, so $1,000 is probably not a realistic amount for her to go home/back 4 times/year minimum (to school, winter break, back to school, home for the summer).

Institutional Aid = Money from the College

- All grants and scholarships are money you don’t have to pay back - we like these in the “Institutional Aid” section.

- Because they come from the college, it’s likely that Gabbie was awarded these as part of this college’s commitment to meet 100% of need. It is also possible that there are requirements to keep the scholarship, like maintaining a certain GPA. Gabbie will have to find out if there are requirements and, if so, make sure to maintain them - her aid will depend on it!

Federal Aid = Money from the Federal government

- Pell Grants come from the federal government and are based on income; you are automatically issued one based on income that you enter on the FAFSA. Grants are free money; no need to repay.

- There are strict penalties for falsifying information on the FAFSA, and I’ve heard that they check about 1 out of 5 of all applicants’ FAFSAs - so make sure you tell the truth!

- The SEOG (Supplemental Educational Opportunity Grant) is based on the FAFSA qualifications. No need to repay; you are automatically , does not need to be repaid, and again, is automatically applied for based on your FAFSA.

- The Federal Subsidized loan DOES need to be repaid; you’ll accrue no interest until 6-9 months after you graduate.

- Work study = on-campus job. The number listed is the maximum amount the college can pay you based on what they have been allotted - so you still have to find a job on campus and work the hours to get paid that money. Often the on-campus job has more money than is listed on your financial aid letter and you can continue working to make a little extra money if you want to - but these jobs pay $7-15/hour, so don’t expect to make a tremendous amount.

- Don't work more than 10-12 hours/week while a full-time college student. You need to study in order to do well, and if you graduate with a low GPA and don’t know the things you are supposed to, you’ll have trouble getting hired and will get quickly fired. Your job is to learn for the time you’re in college; devote yourself to that as you would to a job.

Big Takeaways - Full Ride Financial Aid Letter

- She will owe $1,000/year according to this package. It doesn’t say that anywhere on the letter - that’s math that you have to do yourself.

- Gabbie can negotiate! Maybe she can’t pay 1K/year - she can ask the office of financial aid for more, which they may/may not have.

- How much money can I borrow from the government? (from studentaid.gov, a US government website) https://studentaid.gov/help-center/answers/article/how-much-money-can-i-borrow-federal-student-loans

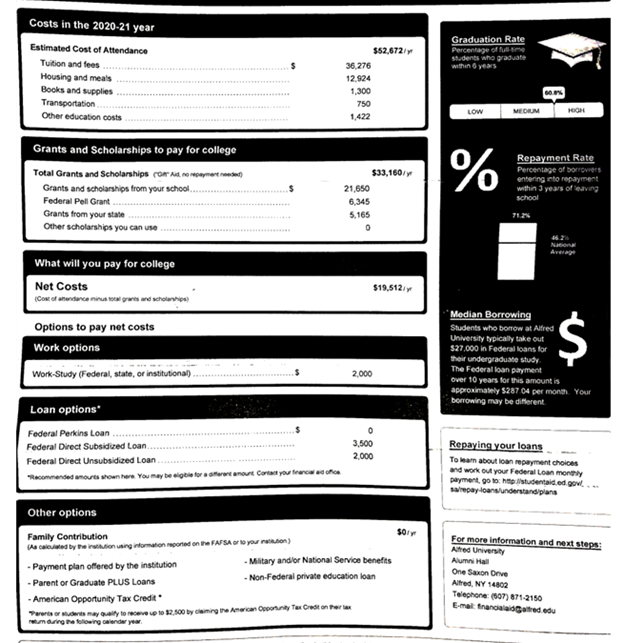

Partial Aid Letter - Alfred University

What You Will Pay for College

- They’ve subtracted the “Estimated Cost of Attendance” and the “Grants and Scholarships” to give you your net cost - and yes this includes room and board - great!

Options to Pay Net Costs

- This letter is done a little differently - it lists options but makes no assumption that you will use them:

- Work Study

- Loans (the $5,500 from the federal government)

- EFC - this school acknowledges that Miguel’s EFC is $0 (his family can’t afford to help with college), but that doesn’t mean they meet 100% of need, unfortunately

- Note that the college doesn’t show Miguel how to pay the whole bill - they list some vague options, but from this letter, there’s no way to pay for the whole thing!

Big Takeaways

- If he takes the work study and the loans, his annual payment will be $19,512 - (2000+3500+2000) = $12,012. This number - $12K - appears nowhere on the letter. That’s math you have to do.

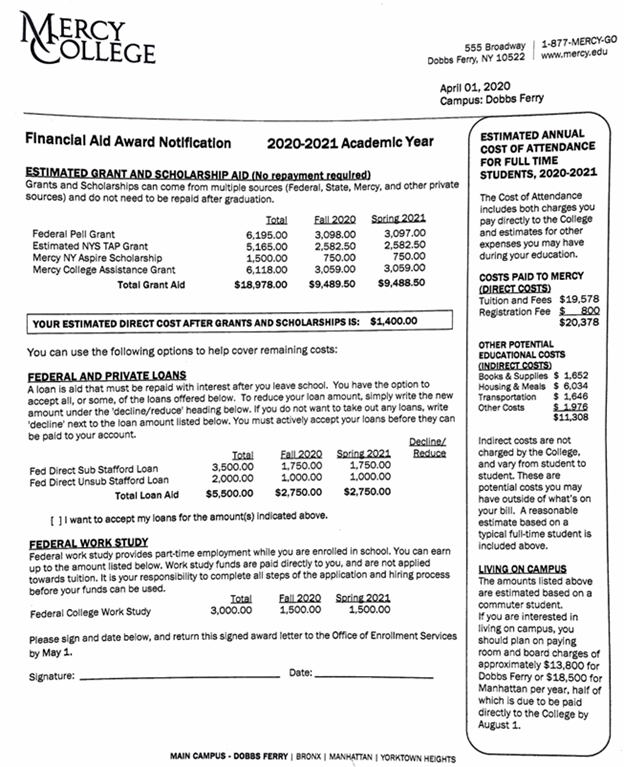

Partial Aid Letter - Mercy College

Estimated Grant and Scholarship Aid

- This has the estimated direct cost after grants and scholarships, which seems like a great price – $1,400!

- But don’t forget the sidebar - they are not including room and board.

- NOTE: The numbers they list as room and board are not what THEY charge, but what they estimate a commuter student should budget. So assuming Miguel wants to live on campus in Dobbs Ferry, there’s another 13.8K that Miguel now has to add to the other listed expenses - which totals to $19,704.

- The $19,704 cost of room, board, books, and more is added to this “estimated direct cost” of $1,400 – his final cost to attend and live on campus is $20,474.

Federal and Private Loans/Work Study

- You can see Miguel’s subsidized and unsubsidized loans

- Miguel was also offered work study

- Accepting these loans and doing work study would decrease his total cost to $11,974

Big Takeaways

- Nowhere in this letter did they do any of the math that Miguel really needed to understand what he was going to PAY!

- They hid the cost of room and board on campus - what looked like a great deal ($1,400) actually ended up being 10 times that ($11,974)! DOING THE MATH IS ESSENTIAL!

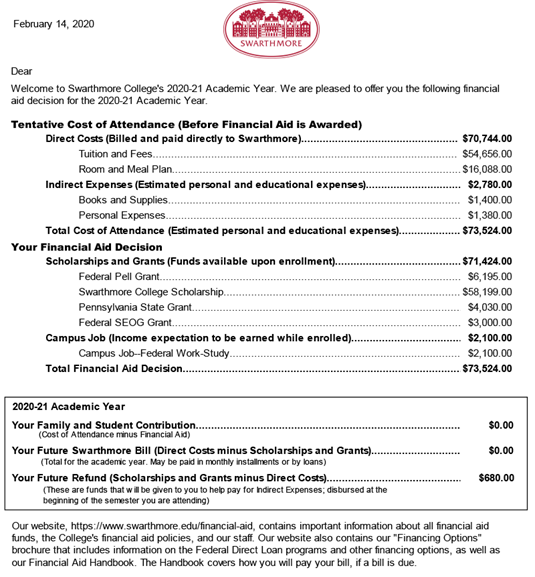

No Loans, Full Ride - Swarthmore College

Tentative Cost of Attendance

- The school lists room and board right up front, as well as books and personal expenses, so Malik knows that everything he needs to worry about has been covered.

- You’ll notice this price tag is extremely high - many families get scared off from the high sticker price of private colleges - but they also have the most $$ to give financial aid.

Your Financial Aid Decision

- Everything that’s on here is money that Malik DOES NOT have to pay back - all grants and scholarships!!!

- The only thing Malik is really responsible for is work study, which means he’ll have to get an on-campus job.

Big Takeaways

- This student will have NO MONEY to pay back after college - “no loan” schools have committed to give students financial aid that will not leave them in debt.

- This student will actually get money at the end, to the tune of $680, in order to help pay the indirect expenses Swarthmore may not have accounted for - because they know things come up!

Financial aid letters run the gamut: Your best bet in navigating them is to ensure you’ve identified:

- Is room and board included in the outlay of costs?

- Are there other specific costs that are specific to your family that you need to make sure you’ve accounted for?

- We strongly suggest you only say yes to $5,500/year in loans (take the federal loans!)

- Make sure you’ve subtracted the cost minus whatever free money and loans you’re going to take.

- You can advocate for more money if you need it - call the financial aid office. There’s often wiggle room - depending on the school, it can be $1-5K.

- If you have questions about the financial aid decision, you can always ask the financial aid office at the school - that’s their job.

- If you’re worried about divulging your identity (eg. you’re undocumented), you can always call and ask a hypothetical question or have a college access person call for you.

- Working with someone with experience in financial aid is ESSENTIAL. These folks can help you make sure you don’t miss anything and fully understand what you’re agreeing to.

Alyssa is the Co-Founder and Executive Director of the Yleana Leadership Foundation, which operates Socratic Summer Academy/SSA Online College Prep. She is a college readiness/admissions expert, known on YouTube as Alyssa the College Expert.

Disclaimer: This blog post was originally published on April 30, 2003. The content has been reviewed and updated for accuracy and relevance in 2026. The original information and guidance were provided by Alyssa the College Expert.

.png?width=352&name=Financial%20Aid%20Money%20(1).png)